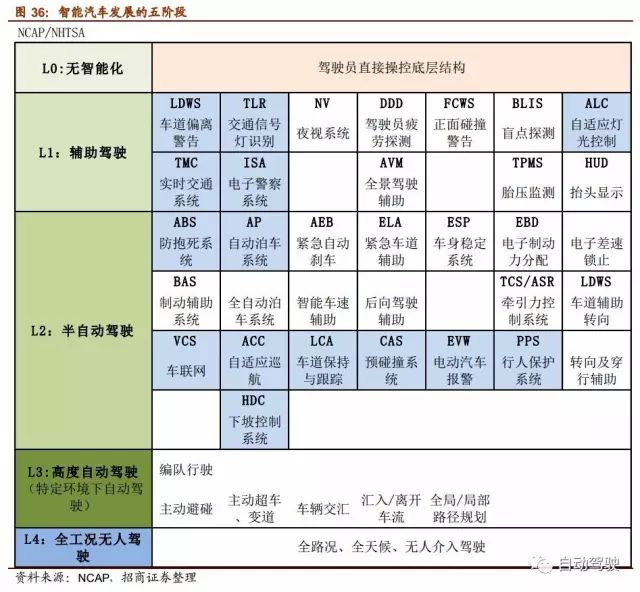

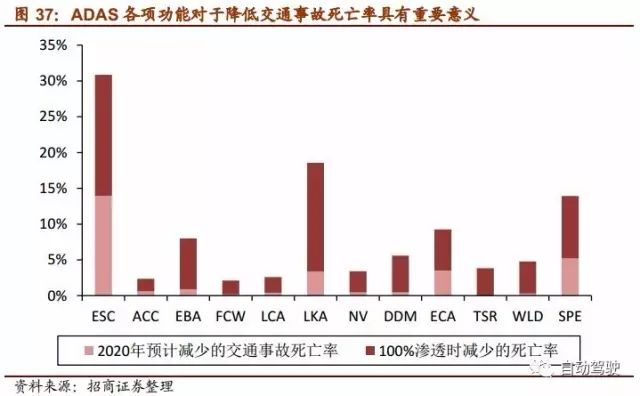

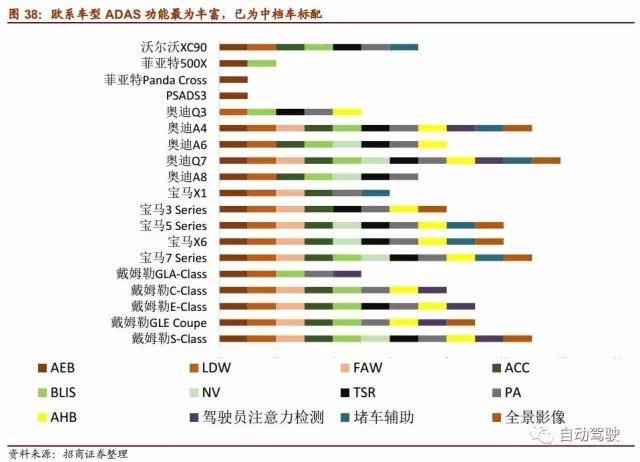

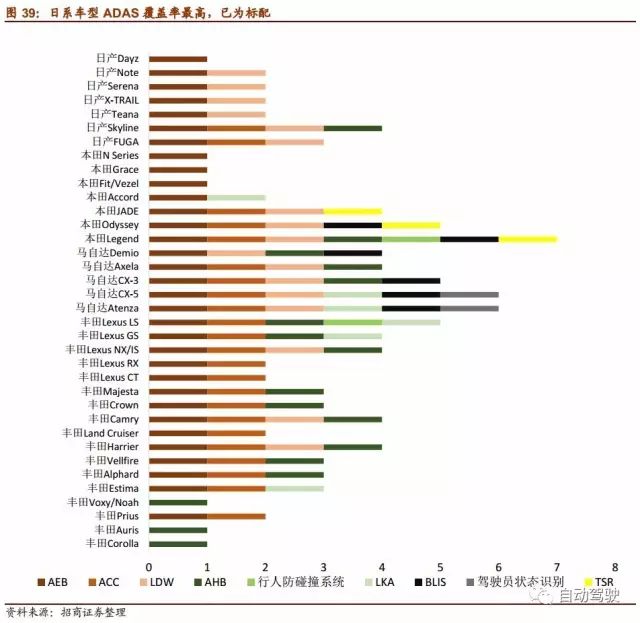

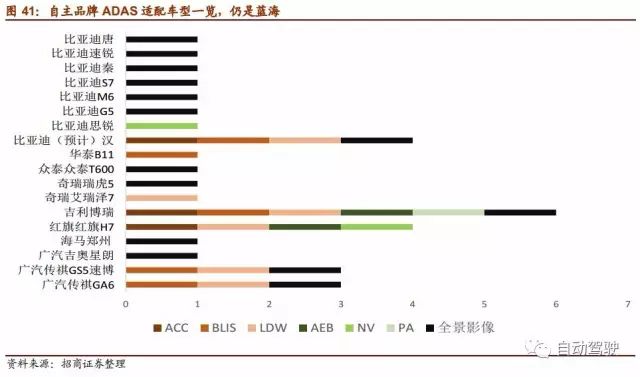

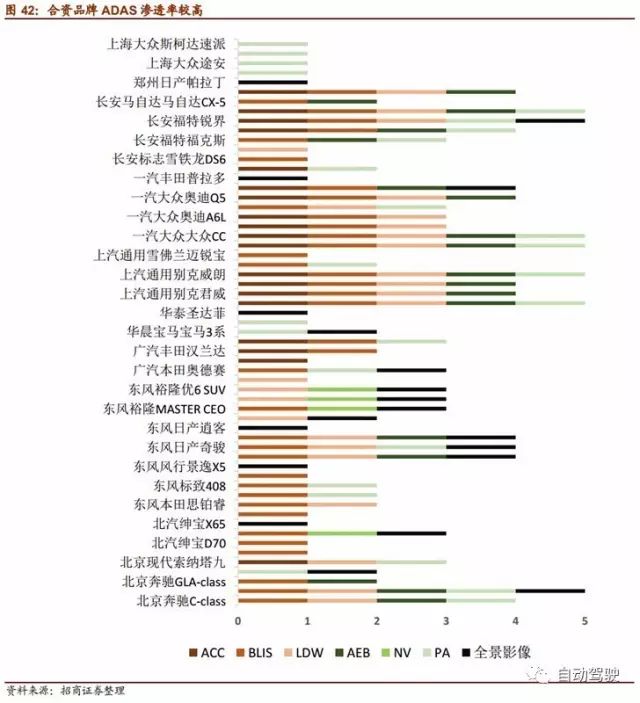

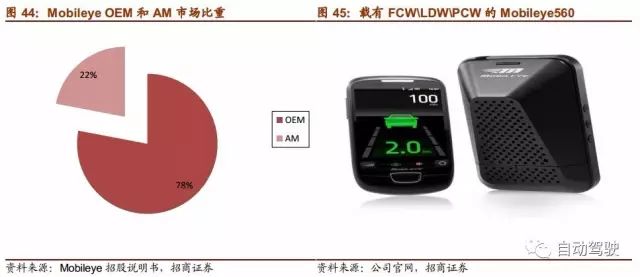

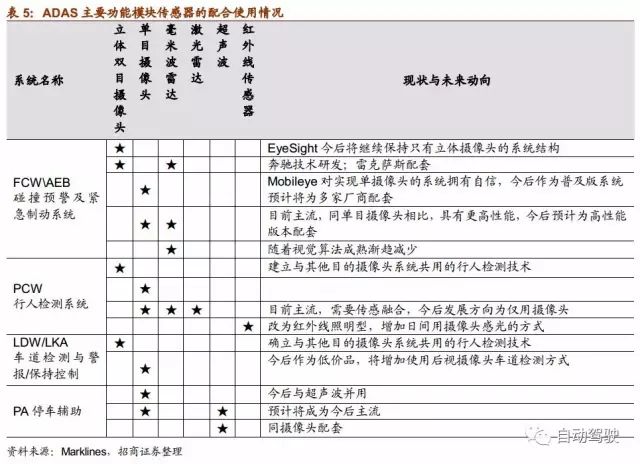

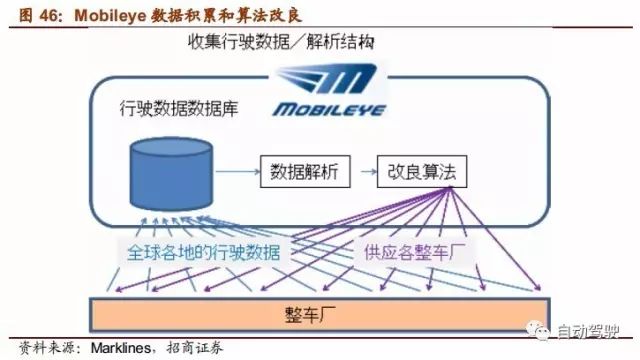

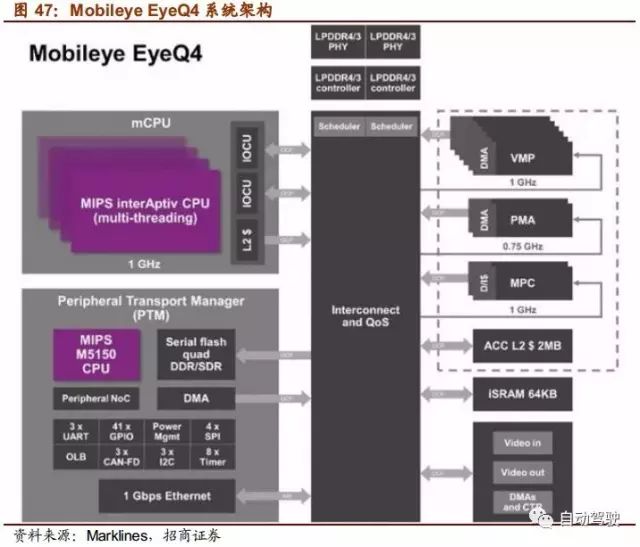

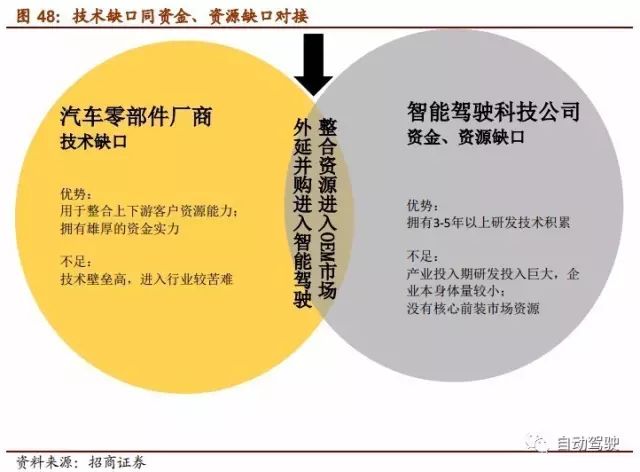

ADAS maturity varies from region to region, but overall it has become the standard for mid- to high-end models. From the perspective of assembly maturity, the European Department> Japanese> US Department> joint venture brands> independent brands, but in addition to independent brands, ADAS core functions ACC, LDW, LKA, PA, BLIS, etc. have become standard in mid-to-high end models. Further expand the trend. As the basic function of smart driving, Assistive Driving has generated over 200 billion yuan of market space for the pan-intelligent driving. As the only road to unmanned driving, assist driving is the basic core link in the industry chain, and it has the radiation effects to all levels of hardware and software, electronics, communications, and machinery. Combined with the forecast of growth rate of 35%, it is estimated that by 2020, the space of the pan-intelligent market will exceed 200 billion yuan. 01 Policies open to the market, opening up the “universal intelligence†market Domestically, the development stage of smart cars is divided into four phases: DA\PA\HA\FA. The stage of international smart cars is divided into the L0-L4 divisions of the US Highway Authority. At present, only the stage of automobile development is at DA\PA or L1\L2. 1. The effectiveness of ADAS is significant, and policies have pushed the market penetration rate to the bottom The ADAS assisted driving system has a strong positive externality. The specific performance is as follows: Significantly reduce the incidence of traffic accidents and deaths. 90% of the mistakes in the driving process are caused by the driver's misoperation. The ADAS system can significantly reduce the driver's misoperation probability. According to e-IMPACT estimates for reducing traffic accident mortality after the installation of the ADAS system, when the ESC penetration rate reaches 100%, the accidental mortality rate can be reduced by 30%, and the LKA (lane retention assistance) can be reduced by 18%. Improve urban operating efficiency and reduce congestion. Congestion on the one hand is limited by the vehicle capacity of the existing road system, on the other hand due to the driver's differentiated driving habits. The speed, lane change, and start-stop control actions vary, and smart driving systems can effectively reduce city congestion and increase urban operating efficiency by 80%. Reduce fuel consumption. The data shows that stop & go automatic start-stop control (part of ACC) can effectively reduce 10-15% of the total fuel consumption. The urban traffic network system can significantly improve the fuel economy performance by 30%-40%. Based on the huge positive externalities, governments of various countries have successively adopted the mandatory form to promote the mandatory assembly of ADAS function modules. National policies and regulations focus on ensuring the basic functions of safe driving: ESC, AEB and TPMS. Second, Europe and the United States and Japan ADAS become standard, the independent brand is still Blue Ocean The European, Japanese and US Department of Automotive ADAS has the highest assembly rate, mainly focusing on high-end models. ACC, LDW, BLIS, PA are the most basic functions. AEB has the highest penetration rate in Europe and Japan. In the United States, there is no mandatory regulation, so it still stays in the FCW phase. European models: ADAS is the most feature rich and has the most mature development. European vehicles are typically represented by ABB, equipped with automatic emergency braking (AEB), lane departure warning (LDW), automatic high beam (AHB), collision warning (FCW), adaptive cruise (ACC), blind spot assistance (BLIS). ), Traffic jam assistance, driver attention detection, night vision assistance (NV), traffic sign recognition (TSR), parking assistance (PA), and panoramic images total 12 ADAS functions. Audi A4, A6, Q7, BMW 3 Series, 5 Series, 7 Series, X6, Mercedes-Benz C-Class, E-Class, and S-Class all achieve 8 or more ADAS functions. The Japanese system followed closely. The Honda system was the most feature-rich and Toyota had the most comprehensive coverage models. The Japanese company is represented by Toyota, Honda, Mazda and Nissan. It covers AEB, LDW, AHB, ACC, pedestrian collision prevention There are a total of nine function modules for BLIS, TSR, driver status recognition, and lane keeping system (LKA). Among them, the Honda system is the most feature-rich and Toyota has the most comprehensive coverage models. Compared with Europe and Japan, the U.S. Department has a slightly lower coverage rate, and its functional modules are mostly 5-6. The U.S. Department is based on GM, Ford, and Chrysler, covering collision warning (FCW), lane departure warning (LDW), lane keeping system (LKA), automatic high beam (AHB), adaptive cruise (ACC), blind spot assistance ( There are eight modules in BLIS, Parking Assistant (PA) and Panoramic Image System. The joint venture has a high coverage of high-end brand ADAS, and its own brand is still Blue Ocean. Among the joint venture brands, the coverage rate of high-end mainstream vehicle models is relatively high. There is no clear regulation in the country to regulate the ADAS function module. Therefore, compared with the European and Japanese systems, the ADAS function of the joint venture brand vehicle system is relatively simple, with adaptive cruise (ACC), blind spot monitoring (BLIS), and LDW (lane departure warning). , panoramic image based. The self-owned brand is still the Blue Ocean, and a very small number of models realize the main function assembly of ADAS. The self-owned brand ADAS has a very low coverage and is based on basic panoramic images. Guangzhou Automobile Chuanqi, Hongqi H7, Geely Borui and upcoming BYD “Han†are the few autonomous models that carry the core functions of ADAS. Taken together, there is still more room for the self-owned brand market. In summary, we conclude that: ADAS maturity varies from region to region, but overall it has become the standard for mid- to high-end models. From the perspective of assembly maturity, the European Department> Japanese> US Department> joint venture brands> independent brands, but in addition to independent brands, ADAS core functions ACC, LDW, LKA, PA, BLIS, etc. have become standard in mid-to-high end models. Further expand the trend. The promotion of regulations and the ADAS assembly rate are directly positively correlated. China has added ESC to the rating item for 15 years and it is worthy of attention. In Europe and Japan, AEB is an ADAS function module that is required by law to be installed. Therefore, AEB is the standard for mainstream vehicles. In the US market, where there is no specific regulation, very few vehicles carry the AEB function, and most of them stay in the FCW collision warning stage. . There is a certain lag period for autonomous vehicles, and the penetration rate in the future is expected to increase substantially. At present, there are still cost-effective resistances to adopting advanced ADAS system modules for self-owned brands. However, with the addition of ADAS systems to benchmark vehicles such as BYDAK, Geeborri, GAC, and so on, basic function modules are expected to be further stimulated in the self-owned brand market. III. The market of ADAS market is 700 billion in 2020, and the space of the pan-smart driving market is over 200 billion yuan. In 2020, the domestic market for assisted driving reached 70 billion, and CAGR exceeded 35%. In China Manufacturing 2025, the National Strategic Advisory Committee has conservatively estimated the penetration rate of assisted driving in 2020 to 50% (facts should exceed 50%), combined with Mobileye's offer of an ADAS warning system and vehicle growth in the next five years, It is estimated that the assist driving market will reach 70 billion in 2020. As the basic function of smart driving, Assistive Driving has generated over 200 billion yuan of market space for the pan-intelligent driving. As the only road to unmanned driving, assist driving is the basic core link in the industry chain, and it has the radiation effects to all levels of hardware and software, electronics, communications, and machinery. Combined with the forecast of growth rate of 35%, it is estimated that by 2020, the space of the pan-intelligent market will exceed 200 billion yuan. 02 Disputes before and after loading: After installing the equipment At this stage, the proportion of the market before and after loading is greater than 4:1, and the application of post-installation products is limited to the early warning level. At present, active safety systems are still concentrated in the pre-installation market. Of the top 10 suppliers in smart driving, only three are involved in both front- and back-loading markets. Taking Mobileye as an example, 78% of its revenue in 2013 came from the OEM market, and only 22% came from the aftermarket. Aftermarket market is mainly reflected in the application of commercial vehicles, insurance companies, fleets and so on. Since the after-installation market has not obtained permission from the host manufacturer's communication protocol, it cannot enter into the implementation level of the ADAS core, and thus the function is more limited to the early warning field. After the installation is limited, the focus of the industry is still pre-installed. Assisting driving is a necessary stage for driving to unmanned driving. The ultimate goal of unmanned driving is to liberate the driver's hands and complete a series of processes of perception, recognition, and decision-making independently through the machine, and ultimately realize highly automated driving. Therefore, "control" is the core of smart driving. Even if the primary ACC, AEB, LKA and other functions are realized through the cooperation of the special system, brake system, and display system. We believe that in the future, the driving force of assisted driving is to involve the simultaneous development of main engine plants and intervene in the CAN bus to realize the synergy integration with other driving functions. With the increase of ADAS's loading rate, the pre-installed market is blue ocean regardless of profit margin or assembly volume. The independent technology company is still in the post-installation warning phase. The cost-effectiveness, accuracy, and response speed are important criteria for this ability to intervene in the pre-installation market stage. According to our industry research on domestic ADAS driving assistance companies, ADAS products of domestic companies are still focused on early warning functions such as FCW, LDW, and PCW. It is mainly equipped with the market for the loading of commercial vehicles and passenger cars. The prices of products are mostly in the range of RMB 1000-2000. At this stage, as the front loading market has not yet started, the single assistance driving function is relatively easy to enter in the aftermarket. However, as the pre-installation technology matures, the cost declines, and the intervention of policy incentives, efforts to cut into the pre-installed market will become the key for technology companies to attack cities. We are optimistic about the first-mover advantage, the strength of the future integration of supply chain resources, through the vehicle factory safety certification cut into the pre-installed market of the company. 03 Technology Path Debate: "Camera + Millimeter Wave Radar" is the Mainstream There are two major technical schools in the Assisted Driving Phase: one is based on pure visual algorithms. Israeli technology company Mobileye occupies more than 80% of the ADAS vision solutions market. Target objects are identified through the "monocular camera + powerful algorithm chip" and are now available. Tesla pre-installed the market and entered the Nissan, Volkswagen front assembly system. The other type is "camera + millimeter wave radar." The camera is used to identify the shape of the object. The millimeter-wave radar is used to measure the distance and supplement the camera's function blind area (such as the detection of object information on rainy days, the identification of animals, the detection of uneven roads, the detection of boundary areas of roads and walls, etc.), This is also the mainstream solution for pre-installing ADAS. Most Tire-1 suppliers and most models will use this method. In contrast, the former has a lower cost, and the algorithm data is a core value, but the accuracy is limited. The latter multi-sensor form accuracy is guaranteed, but the cost is high, and the radar module has a large size, which needs to be synchronized with the vehicle manufacturer for embedded development. First, the pure vision plan: The application scene is limited Mobileye is the spokesperson for visual algorithms, with advantages in data and algorithms. Israeli high-tech company Mobileye has more than 80% market share in visual algorithms. Its long-term data accumulation and algorithm optimization are core competitive advantages. Custom visual processing GPU chip. In cooperation with STMicroelectronics, STMicroelectronics has developed a carrier chip specifically designed for visual algorithms and has a GPU (Process Image Information) + CPU (Process Data Algorithm Information) processing capability. Use data accumulation improvement algorithm. Establish a vehicle driving database developed with the camera to continuously improve the optimization algorithm. Mobileye has the most comprehensive database of terrain and climate image information. Through analysis, it extracts improved recognition algorithms. The database that is accumulated through a large amount of road information is a core advantage of Mobileye. Simply relying on a monocular camera to achieve full functionality in the ADAS stage is Mobileye's goal. The monocular camera still has many deficiencies: The continuous expansion of the identification range, identification space, and application scene is the direction of future technology. The range of identification objects is limited. Currently identifiable areas include vehicles in front, pedestrians, obstacles, light sources (headlights, taillights), speed limit signs. For the time being, we cannot rely on single cameras to identify animals, traffic signs (various shapes), traffic lights, etc. Unable to detect depth of field. The depth map is obtained by the monocular camera, and the bump detection of the road is performed (the change of the step of the sidewalk is detected). Insufficient distance and speed adaptation. Compared with millimeter wave radar, camera distance measurement is not stable. At the same time, the ADAS module is far less adaptable to speed than radar. Second, "camera + millimeter wave radar": cost, accuracy, speed, balanced solution Assisted driving stage cameras, millimeter-wave radar, and laser radar are commonly used object recognition sensors. Purely visual algorithms are basically sufficient for Mobileye's early warning function. However, the accuracy becomes insufficient from the early warning to the execution level. The fault tolerance of the vehicle for reverse control is very low, which requires at least two kinds of sensor information for redundancy verification, to achieve improved accuracy, and at the same time, to meet the backup solution when a sensor function is damaged in extreme weather. "Camera + Millimeter Wave Radar" program: The optimal choice between cost, accuracy, and speed. "Camera + millimeter wave radar" or "camera + laser radar" is a method that can be selected under the accuracy guarantee. The laser radar has the highest accuracy and the error is in the centimeter level. At the same time, it can scan the outline of objects and provide accurate speed, distance information, and 3D maps. However, the cost of several hundred thousand yuan is hard to commercialize. Therefore, "camera + millimeter wave radar" has become a cost-effective choice. The price advantage is obvious. The camera detects the shape, the millimeter-wave radar measures the distance and velocity, and tracks the object's trajectory with complementary advantages. With the optimization algorithm, it can cope with the driver's execution layer needs. At the same time, the camera cannot recognize the animals or the uneven road surface and cannot be used in rain, snow or fog, and the millimeter-wave radar has less limited application scenarios. Mobileye's EyeQ4 product, which will be available in 2017, will be equipped with 3 cameras and radar and laser detection equipment around the vehicle body to achieve semi-autonomous driving on the highway. In the execution layer application, the camera + multi-sensor gradually becomes mainstream. Reverse promotion algorithm speeds up. "Complementary advantages" is the optimal path choice for assisted driving. The cost of a millimeter-wave radar is around $30, and the price/performance ratio has prompted it to become the mainstream choice for OEMs. At the same time, the information fusion of camera and millimeter-wave radar is more conducive to the process of feature extraction and foreground separation, and the speed of the algorithm is improved. 04 Industry Opportunity: Outreach and Short-term M&A, Pre-loading Opportunity Time accumulation: It is a technical barrier in the field of smart driving. As a technology-intensive industry, smart driving is a long process from R&D, experimentation, correction, and industrialization. Mobileye has been developing vehicle and pedestrian identification systems since 2000, after 16 years of algorithm optimization and data accumulation to form products. Google also completed preliminary product development after nearly 10 years of algorithmic data improvements. The technological development of domestic smart driving lags behind Europe, the United States, Japan and other countries and regions, but benefit from the peripheral technology-driven development investment is much less than the original development. Extensive mergers and acquisitions: domestic parts manufacturers cut into the field of smart driving shortcuts. We believe that there are two gaps in the domestic smart driving industry: 1. Traditional OEMs and parts factories lack relevant experience and there is a technological gap, but there are sufficient funds. 2. Technology companies with core technologies are often too small to support the high cost of R&D. However, some companies currently have the pre-installation conditions. The strong demand for complementary resources determines that outsourcing will become the best way for domestic manufacturers to get involved in the smart driving industry. The entrance to the platform is an investment focus, and the pre-installation is the core catalyst. It is unlikely that an OEM will directly cut into the development of a full-featured smart driving system. Just like our analysis of Google, development at the implementation level is as difficult as the identification level. The best bridging platform between OEMs and technology companies is A large number of accessories companies that continue to transform, such as brake systems, power or conventional systems, and traditional manufacturing companies such as HMI. At present, the domestic technology side is basically confined to the ADAS primary function development in the aftermarket, and it has not been able to cut into the front-loading core manufacturers and core models. Therefore, the highlight of this phase of investment should be a spare parts transition company that intends to expand in an extended manner into the ADAS sector. Relying on existing OEM resources, the front-loading market will become the core catalyst for the 16-year industry.

With the improvement of people's quality of life, people's lifestyles have also become varied. Different kinds of recreational products are starting to appear in people's lives, such as electronic cigarettes. The emergence of e-cigarettes represents a part of young people's thinking and means that electronic products are beginning to show a trend towards diversity.

simply replace the pods. The Pod system uses an integrated pod rather than a tank for higher nicotine strength and provides low power traction. the Pod system is rechargeable and has a longer life and higher battery capacity than disposable electronic cigarettes.

Our company Pod system has a built-in 380mAh battery and a USB charging port on the bottom. In comparison, the Pod system has a built-in battery of only 180mAh, but the Pod system charges much faster.

Our electronic cigarettes are of rechargeable construction. The first time you use the charger to charge, it is recommended to use up the remaining power before filling up, this is to ensure the performance of the battery.

Vape Pod System Oem,Vape Pod Oem,Close Pod Oem,Thc Pod Disposable Shenzhen MASON VAP Technology Co., Ltd. , https://www.disposablevapepenfactory.com